Every few months, I get a question about whether VTIP is “still cheap” and if it “still makes sense.” Right now, with where inflation expectations, real yields, and the bond market overall stand, this is absolutely a legitimate question that’s worth more than a quick, knee-jerk “yes” or “no.”

Here’s a breakdown of what the data actually says, where VTIP belongs in a portfolio, and whether it’s an appropriate asset for you.

What Exactly Is VTIP?

But before we get into the yield calculations, a bit of background: VTIP is the Vanguard Short-Term Inflation-Protected Securities ETF, established in October 2012. It is designed to track the investment performance of U.S. Treasury inflation-protected securities (TIPS) with maturities of fewer than five years.

Emphasis on short-term. This ETF is not looking to be the most exciting inflation protection on the market. It’s a fine-tuning tool-a way to have your cash linked to CPI without exposing it to the duration risk which is so detrimental to long-term TIPS funds when real rates increase.

In April 2026, VTIP had an average effective duration of about 2.4 years. This is considered short duration for this type of investment and more important than investors might expect. It’s time I explain why.

The Dividend Yield Picture — And Why It’s Complicated

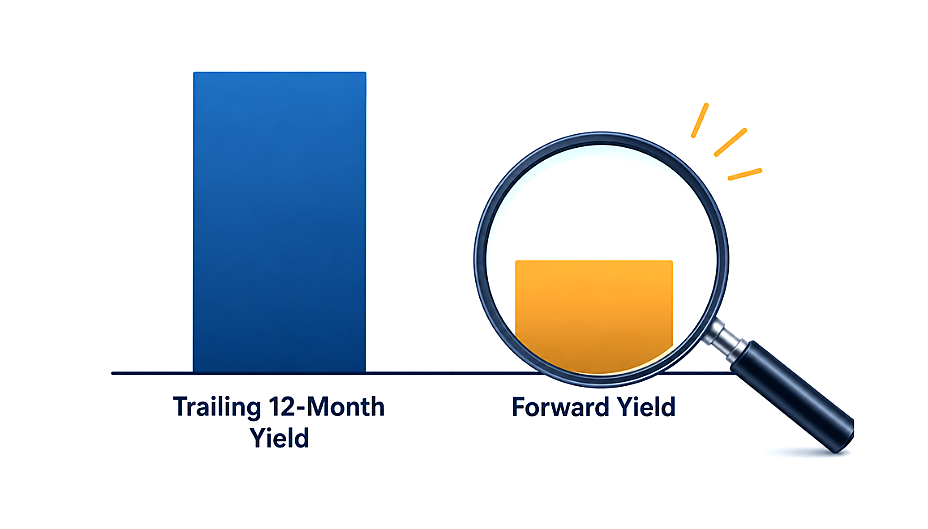

Here’s where you need to be careful. Because it’s easy to get two very different pictures of VTIP’s dividend yield from data aggregators.

Most of the data providers will show VTIP yielding somewhere between 3.59% to 3.63% on a TTM basis. That might sound attractive–a yield substantially higher than an average short-term Treasury fund. However, the annualized forward yield (based on the latest quarterly payout) is closer to 0.18%.

This is not a typo. This gap is indicative of how TIPS distributions actually work.

TIPS payouts consist of a fixed coupon rate plus an adjusted portion based on CPI increases (or decreases). With the massive inflation seen throughout 2022 and 2023, those CPI adjustments inflated those distributions quite a bit. With cooler inflation and lower CPI adjustments since then, the quarterly payouts have shrunk substantially-the last quarterly payout was a mere $0.0227 per share paid on April 6, 2026.

So when someone tells you VTIP yields 3.6%, they're largely describing what happened over the past year, not what you should expect to collect going forward at the current run rate. The forward yield is the more honest guide to near-term income.The Real Return Argument

Here’s the case that veteran TIPS investors actually make — and it’s stronger than the dividend story.

VTIP’s total return is effectively designed to equal the real yield on short-term TIPS plus CPI inflation. A recent analysis from Seeking Alpha put VTIP’s expected forward returns at roughly 1.1% above inflation — which, if you’re running at something close to current CPI levels, translates to a total return in the neighborhood of 4.9%.

That is not bad for a fund with zero credit risk, almost no duration risk, and an expense ratio of just 0.03% — one of the cheapest in any bond category.

A $10,000 investment in VTIP since inception has grown to approximately $13,663 as of April 30, 2026, versus $11,800 for the Bloomberg U.S. Aggregate Bond Index over the same period. For a “boring” government bond fund, that’s a meaningful margin.

How VTIP Stacks Up Against the Competition

The three names that always come up in this comparison are VTIP, SCHP, and TIP.

VTIP vs. SCHP (Schwab U.S. TIPS ETF): Both carry a rock-bottom 0.03% expense ratio. The meaningful difference is duration. SCHP covers the full TIPS curve with a duration of roughly 7–8 years, versus VTIP’s 2.4 years. That longer duration gives SCHP more upside if real rates fall — but it also means more pain if they rise or stay elevated. SCHP’s volatility runs at 0.92% versus VTIP’s 0.47%, and SCHP’s maximum drawdown since inception was -14.26%, compared to VTIP’s far more restrained -6.27%. VTIP’s Sharpe ratio over the past twelve months of 2.90 also looks significantly better than SCHP’s 1.48.

VTIP vs. TIP (iShares TIPS Bond ETF): TIP has higher liquidity and over $30 billion in AUM, but it charges a notably higher 0.19% expense ratio and carries similar long-duration risk to SCHP. Over a long holding period in a tax-advantaged account, that fee difference compounds into a real performance gap.

For investors who do not want to bet on the direction of long-term real rates — and in a market where the 30-year yield has been trading north of 5%, that’s a reasonable position to hold — VTIP is the cleaner instrument.

Who Should Own VTIP Right Now?

Let me be direct about who this fund is and isn’t designed for.

VTIP makes sense if you:

- Want a pure, low-risk inflation hedge without meaningful interest rate sensitivity

- Are in or near retirement and prioritize capital preservation over yield maximization

- Hold a diversified fixed income sleeve and want to offset nominal bond exposure

- Believe inflation will remain sticky or trend higher, and want a responsive (short-duration) way to capture that

- Are building a conservative IRA allocation where fee drag compounds over decades

VTIP may not be the right fit if you:

- Need predictable, consistent quarterly income — the distribution volatility tied to CPI adjustments makes VTIP unreliable for income planning

- Are chasing yield and see the 3.6% TTM number without understanding it likely overstates forward income

- Have a long time horizon and can stomach more duration risk for potentially higher real-yield upside via SCHP or similar

The Inflation Context for 2026

The macro backdrop matters here. The tariff-driven inflation narrative that re-emerged in late 2025 and early 2026 has kept inflation expectations elevated even as actual CPI readings have been choppy. A recent piece on ETF.com noted that with the 30-year yield trading above 5%, duration risk in long-bond funds is a genuine concern — which is precisely why short-duration TIPS instruments like VTIP have attracted renewed interest.

The fund has seen net inflows of approximately $4 billion over the past year, which suggests institutional and retail money is actively making this rotation. That kind of flow data is rarely noise.

Morningstar’s April 2026 analysis noted that VTIP’s muted credit risk profile has historically held up well during credit shocks — citing March 2020 as a reference point — and that its low 0.03% expense ratio should help it maintain a performance edge over more expensive category peers.

A Note on Tax Treatment

One thing that catches investors off guard: TIPS principal adjustments are taxable as ordinary income in the year they occur, even though you don’t actually receive that cash — it’s added to the bond’s principal. This phantom income issue makes VTIP considerably more tax-efficient when held inside a tax-advantaged account (IRA, 401k) versus a taxable brokerage. If you’re holding VTIP in a taxable account, that’s not disqualifying, but it’s something to model out with your tax advisor.

The Bottom Line

VTIP is not a yield story. The trailing yield numbers look attractive on a screener, but the forward income picture is much thinner and far more variable than a traditional bond fund.

What VTIP actually delivers — and does it better than almost any comparable instrument — is low-cost, low-volatility, real-return protection against inflation. With a 0.03% expense ratio, a maximum drawdown that’s less than half of longer-duration TIPS funds, and the full backing of the U.S. Treasury, it earns its place in a carefully constructed portfolio.

The question isn’t whether VTIP’s dividend yield is worth it. The better question is whether what VTIP actually does is worth it for your specific situation. For conservative investors, retirees, and those building inflation resilience without taking on duration risk in a still-elevated rate environment — the answer is yes.

For yield hunters who want to see 4–5% consistent distributions? Look elsewhere, and know what you’re trading away to get it.