Buying your first asset before the age of 30 is one of the most powerful financial moves you can make. It doesn’t require a windfall inheritance or a six-figure income. The truth is much simpler: with the right financial habits and a clear strategy, you can buy your first asset using only your salary.

The people who build real wealth before 30 don’t necessarily earn more than you — they just start using their money differently, and they do it early. In this guide, you’ll learn exactly how to buy your first asset before 30, even if you’re earning an average salary.

What Exactly Is an “Asset”?

Before we talk about how to buy your first asset before 30, let’s define what we’re actually talking about.

An asset is anything that puts money in your pocket — either by generating income, appreciating in value over time, or both. The classic examples include:

- Real estate (rental properties)

- Stocks and index funds

- Bonds

- A business or side business

- Digital assets (websites, content platforms, royalty-generating products)

- REITs (Real Estate Investment Trusts — more on this below)

The opposite of an asset is a liability — something that takes money out of your pocket. A depreciating car you financed at a high interest rate? Liability. A credit card balance you carry every month? Liability. Understanding this distinction is the foundation of building wealth.

Robert Kiyosaki made this concept famous in Rich Dad Poor Dad, but the principle is timeless: wealthy people accumulate assets; others accumulate liabilities while thinking they’re assets.

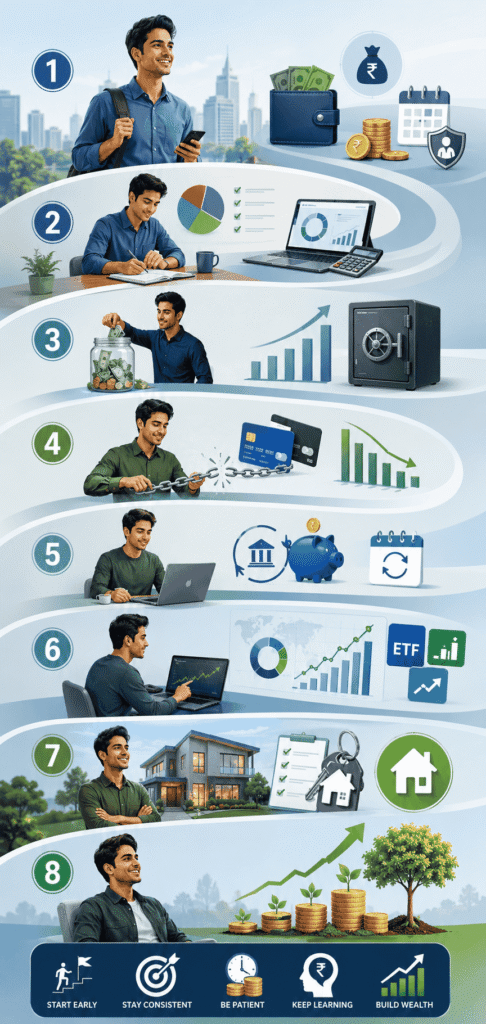

Step 1: Calculate Your Current Financial Position

Before you can buy anything, you need to know exactly what you’re working with. In simple words buying your first asset before 30 is understanding your finances.

Ask yourself:

- How much do I earn monthly?

- What are my fixed expenses?

- How much debt do I have?

- How much can I save consistently?

Create a simple budget with three categories:

Needs

- Rent

- Utilities

- Transportation

- Food

Wants

- Entertainment

- Dining out

- Shopping

Savings and Investments

- Emergency fund

- Asset acquisition fund

Many financial advisors recommend saving at least 20% of your monthly income if possible.

Step 2: Build an Emergency Fund First

If you jump into investing without an emergency fund and something goes wrong (job loss, medical expense, car breakdown), you’ll be forced to sell your assets at the wrong time, possibly at a loss.

Before purchasing assets, build an emergency fund covering:

- 3 to 6 months of living expenses

This fund protects you from unexpected events such as:

Medical emergencies

- Job loss

- Car repairs

- Family obligations

Without an emergency fund, you may be forced to sell your assets at the wrong time.

Step 3: Eliminate High-Interest Debt

If you have credit card debt or other high-interest loans, prioritize paying them off.

For example:

If your credit card charges 25% annual interest, earning 8% from an investment won’t compensate for that loss.

Focus on:

- Paying off high-interest debt first

- Avoiding unnecessary borrowing

- Improving your credit profile

Once your debt is under control, you’ll have more money available to purchase assets.

Step 4: Automate Your Savings

One of the most effective wealth-building habits is paying yourself first.

Set up an automatic transfer from your salary account immediately after payday.

For example:

- Monthly Salary: $2,000

- Automatic Savings: $400 (20%)

Over one year, you’ll accumulate:

$400 × 12 = $4,800

Without relying on willpower.

Automation removes emotional spending decisions and keeps you focused on your goal.

Step 5: Choose the Right Asset for Your Income Level

Here’s where a lot of young professionals get stuck — they think buying an asset means buying a house or apartment, which requires a huge down payment they don’t have. The truth is, there are multiple types of assets you can start with on a modest salary.

Option A: Stock Market Index Funds (Best for Beginners)

If you’re new to investing, index funds are arguably the most accessible, lowest-risk entry point for a salaried individual. An index fund tracks a market index (like the S&P 500 or Pakistan Stock Exchange index), which means you’re essentially buying a small slice of many companies at once.

Why index funds work well for salary earners:

- You can start with very small amounts

- No need to pick individual stocks

- Historically, index funds outperform most actively managed funds over long periods

- You can set up automatic monthly contributions aligned with your salary

Platforms like brokerage accounts or apps make this incredibly simple. You set a recurring investment on payday — even PKR 5,000 or 10,000 per month — and let it grow.

Option B: Real Estate Investment Trusts (REITs)

Don’t have enough for a down payment on property? REITs let you invest in real estate without buying physical property. They’re companies that own income-generating real estate (malls, apartments, office buildings) and are traded on the stock exchange like regular shares.

REITs typically pay dividends, which means regular passive income. They’re a great way to get real estate exposure with a small initial investment.

Option C: A Small Business or Side Income Asset

Some people prefer to build an asset they control directly. This could be:

- A freelance service turned into a proper business

- A content platform (YouTube channel, blog, newsletter) that generates ad or sponsorship revenue

- An e-commerce store with low startup costs

- A digital product (course, template, e-book) that earns royalties

These take more effort to build, but the upside is that you’re creating something with tangible long-term value — and the startup costs are often very low.

Option D: A Rental Property (With Smart Financing)

This one requires more capital, but it’s absolutely achievable before 30 if you’re disciplined. The key is to start with affordable property in a growing area, use financing wisely, and ensure the rental income covers or exceeds your mortgage payment.

Many people buy their first rental property by:

- Saving aggressively for 2–3 years

- Choosing a smaller, more affordable unit in a high-demand rental area

- House-hacking (living in part of the property and renting out the rest)

If property prices in your city feel out of reach, look at lower-cost cities or residential plots in developing areas that are likely to appreciate over 5–10 years.

Step 6: Increase Your Income to Accelerate the Process

Buying your first asset before 30 becomes much easier when you increase the gap between income and expenses.

Ways to increase your savings rate:

Reduce Lifestyle Inflation

When your salary increases:

- Avoid upgrading everything immediately

- Save a portion of every raise

Cut Unnecessary Expenses

Review subscriptions, memberships, and impulse purchases.

Ask yourself:

“Does this purchase move me closer to my financial goals?”

Negotiate Bills

You may be able to lower:

- Internet costs

- Insurance premiums

- Utility expenses

Small savings accumulate significantly over time.

Step 7: Think Long-Term

One reason many young investors fail is impatience.

Building wealth takes time.

Avoid:

- Chasing quick profits

- Following social media hype

- Making emotional investment decisions

Focus on:

- Consistent investing

- Regular contributions

- Long-term growth

The most successful investors often succeed because they stay invested for years.

Common Mistakes to Avoid

Many young people sabotage their asset-building efforts without even realizing it. Watch out for these:

• Lifestyle inflation: Every time you get a raise, upgrading your lifestyle proportionally means you never save more. Keep your expenses relatively stable as your income grows.

• Buying a car on debt: A financed car is a double liability — it depreciates while you pay interest. If you need a car, buy what you can afford outright or keep the loan very small and short.

• Waiting to “have more money”: There’s never a perfect time. Start with what you have, even if it’s small.

• Getting distracted by get-rich-quick schemes: Crypto gambling, penny stocks, pyramid schemes — these destroy wealth far more often than they build it. Stick to boring, proven asset classes.

• Not diversifying: Don’t put everything into one asset. Spread your risk across stocks, some real estate exposure, and possibly a small business or side income.

Final Thoughts

If you’re wondering how to buy your first asset before 30, remember that the process is less about earning a huge salary and more about managing the income you already have.

Start by creating a budget, building an emergency fund, eliminating high-interest debt, and consistently saving a portion of your salary. Then invest in assets that align with your financial goals and risk tolerance.

The earlier you begin, the more time your money has to work for you.

Call to Action

Are you planning to buy your first asset before 30? Start by reviewing your budget this week and identifying one change that can increase your monthly savings. Small actions taken consistently can lead to extraordinary financial results over time.

1 thought on “How to Buy Your First Asset Before 30: Using Only Your Salary”