Most people don’t struggle financially because they lack income. They struggle because they lack systems.

According to research from the Federal Reserve, many adults would still find it difficult to cover an unexpected expense without borrowing money or selling something. This highlights an uncomfortable truth: financial security isn’t determined solely by how much you earn. It’s heavily influenced by how you manage what you earn.

The good news? Money management habits are learnable.

In this guide, you’ll discover practical strategies how Smart Money Management Habits Can Transform Your Finances, and how to build them without turning your life upside down.

Why Money Management Habits Matter More Than Income

Many people assume financial success starts with a higher salary. While income certainly helps, it rarely solves poor financial behavior.

Consider two individuals earning the same amount. One spends impulsively, carries credit card debt, and saves inconsistently. The other follows a budget, invests regularly, and tracks expenses carefully.

Five years later, their financial situations can look completely different.

Financial habits compound in much the same way investments do. Small actions repeated consistently create significant outcomes over time. This principle forms the foundation of successful personal finance.

The Real Goal: Financial Control

Money management isn’t about restricting every purchase or eliminating enjoyment. It’s about gaining control over your finances so your money supports your goals rather than creating stress.

The habits below focus on creating that control.

Core Money Management Habits Worth Building

1. Pay Yourself First — Before You See the Money

This is the oldest trick in personal finance, and it’s old because it works. The moment your paycheck lands, a pre-set transfer moves a fixed amount into savings or investments — before you can spend it. What’s left is your ‘real’ budget.

The psychological effect is significant. When savings come off the top automatically, you adapt your spending to what remains. The reverse — trying to save what’s ‘left over’ at the end of the month — almost never works because there’s rarely anything left.

📊 Quick Stat

A Vanguard study found that participants who used automatic contribution increases saved 3x more over a 10-year period than those who manually adjusted their savings rate.

Start small if needed — even 5% of income automated is infinitely better than 20% intended. Increase the amount by 1% every three months and most people never notice the difference in their take-home pay.

2. Use a Zero-Based Budget — At Least for One Month

Zero-based budgeting means assigning every dollar a job until your income minus your allocations equals zero. Not because you’re spending everything, but because every dollar has an intentional destination — including savings and investments.

You don’t have to do this forever. Running a zero-based budget for even one month is extraordinarily revealing. Most people discover two or three spending categories where money was simply leaking without any conscious decision behind it — subscriptions, convenience spending, impulse categories.

Apps like YNAB (You Need A Budget) are built around this method. Traditional spreadsheets work equally well. The tool matters less than the discipline of doing the exercise.

3. Build the 24-Hour Rule Into Any Discretionary Purchase

Impulse spending is the silent killer of most financial plans. The fix is simple and almost insultingly low-tech: wait 24 hours before buying anything that isn’t essential and wasn’t planned.

What happens in that 24 hours? The dopamine spike from the discovery of something new fades. You evaluate whether you actually want the thing, or just wanted the feeling of buying it. Most non-essential purchases either get forgotten or reveal themselves as something you genuinely need — in which case, buy it.

For higher-ticket items, extend the wait to 72 hours or a week. The rule scales.

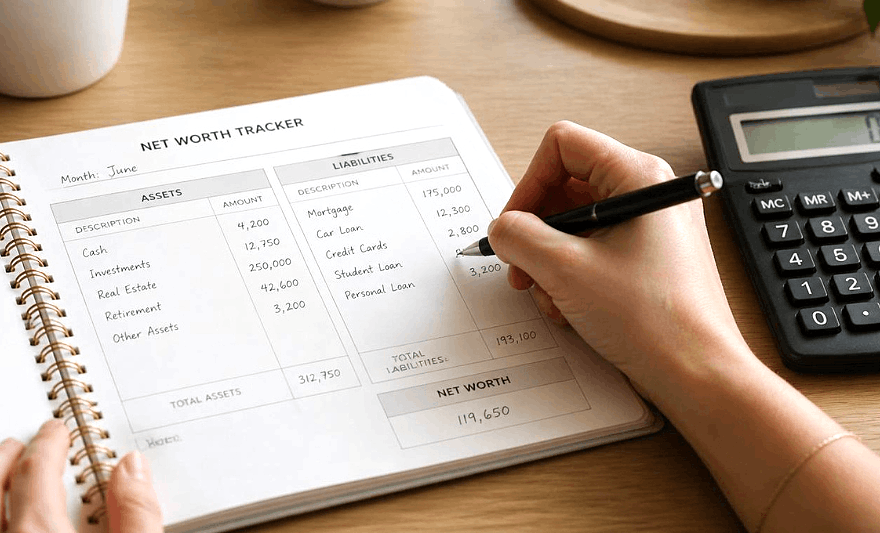

4. Track Net Worth Monthly — Not Just Your Balance

Checking your bank balance is like judging your fitness by how much you weigh today. It’s one data point, stripped of all context.

Net worth — assets minus liabilities — is the actual scorecard of financial health. It accounts for debt paydown, investment growth, retirement contributions, and the equity you’re building. A person with $3,000 in their checking account and $50,000 in a retirement fund is in a fundamentally different position than someone with $3,000 and $40,000 in student debt.

Tools like Personal Capital (now Empower), Monarch Money, or even a simple spreadsheet can automate this calculation. Track it monthly. Watch it trend over 12 months. That trend line will tell you more about your financial trajectory than any single snapshot.

5. Build a Financial Firewall Between Checking and Savings

Convenience is the enemy of saving. If your savings account is at the same bank as your checking account and accessible with one click, you’ll raid it. That’s not a character flaw — it’s how the human brain responds to readily available options.

Move your emergency fund and medium-term savings to a separate high-yield savings account, ideally at a different institution. The minor friction of a 1–2 day transfer delay works surprisingly well as a psychological barrier. Out of sight, out of reach, out of mind — in the best possible way.

High-yield savings accounts currently offer 5% APY (as of mid-2026) , compared to the national average of around 0.46% at traditional banks. That difference compounds meaningfully over years.

6. Automate Bill Payments — But Review Them Quarterly

Auto pay for recurring bills eliminates late fees and the mental overhead of remembering due dates. But it has a dark side: it also removes the regular reminder that you’re paying for something.

The fix is a quarterly billing audit. Set a calendar reminder every three months to review every auto-paying subscription and bill. The question for each one: Am I getting value proportional to what I’m paying? You’ll find services you forgot existed, overlapping subscriptions, and recurring charges that have quietly increased.

Most people who do this for the first time find $50–$200 in monthly expenses they can eliminate without any meaningful loss of quality of life.

7. Invest in Index Funds Before You Try to Get Clever

This is the section where most personal finance articles pivot to sophisticated investment strategies. We’re not going to do that.

The research on active investing vs. passive index fund investing is conclusive: over a 10-year period, approximately 85–90% of actively managed funds underperform their benchmark index, after fees. For most retail investors, a simple three-fund portfolio — total US market index, international index, bond index — outperforms complex strategies because it has lower costs and avoids the behavioral mistakes that come with active management.

Warren Buffett himself has instructed the trustee of his estate to put 90% of his wife’s inheritance into a low-cost S&P 500 index fund. If that’s good enough for Buffett’s estate planning, it’s worth taking seriously.

💡 Key Insight

The unsexy truth about building wealth: time in the market beats timing the market. A $500/month investment in a total market index fund, started at age 25 and maintained until 65, grows to approximately $1.7 million at a 7% average annual return. The strategy isn't complicated — the execution is.

The Habits That Protect What You Build

Maintain Adequate Insurance Coverage

Financial planning is usually discussed in terms of accumulation — earning, saving, investing. But wealth destruction happens fast, and the most common accelerant is inadequate insurance.

A single uninsured medical event can erase years of savings. A disability — statistically more likely than most people assume, with roughly 1 in 4 workers experiencing a disability before retirement age — can destroy income for months or years. Life, disability, health, and liability coverage aren’t expenses; they’re structural protection for everything else you’re building.

Schedule a Monthly Money Date With Yourself

One underrated smart financial habit: treat your monthly financial review like a meeting you can’t cancel.

Set aside 30–45 minutes each month to review last month’s spending against your budget, check your net worth, confirm investment contributions went through, and set one specific financial goal for the coming month. No multitasking, no distractions.

This habit alone — consistent, scheduled financial attention — separates people who eventually achieve their financial goals from those who perpetually intend to but never quite get there. Attention is the most undervalued financial tool.

Building the System, Not Just the Knowledge

Here’s what most financial education gets wrong: it focuses on what to know instead of what to build. Knowing that you should invest early is useful. Having automatic monthly transfers to an index fund is transformative.

The money management habits in this article aren’t secrets. None of them require a finance degree, a high income, or perfect discipline. They require design — setting up systems that make the right behavior the default, not the exception.

Start with one habit. Pick the one that addresses your biggest current vulnerability — whether that’s spending leakage, no emergency fund, or missing out on years of investment growth. Implement it this week. Then add another in 60 days.

Financial transformation isn’t a single decision. It’s the accumulation of small, consistent, well-designed choices made over time. That’s always been true. The people who build real financial security aren’t necessarily smarter or more disciplined — they’ve just built better systems.

Build the system. The results follow.

Conclusion

Strong finances aren’t built through luck. They’re built through consistent behavior.

The most effective money management habits—tracking expenses, budgeting wisely, building emergency savings, automating investments, eliminating debt, and continuously improving financial literacy—work because they create systems that support long-term success.

You don’t need to implement every habit immediately.

Choose one habit this week. Master it. Then add another.

Over time, these smart financial habits can completely transform your relationship with money and create lasting financial security.

Personal finance is less about perfection and more about progress. Small improvements made consistently often outperform dramatic changes that don’t last.

Start today. Your future self will thank you.

1 thought on “Smart Money Management Habits That Can Transform Your Finances”