Let’s be honest. Most of us were never taught how money actually works. School covered algebra and history, but not how to build a budget, escape debt, or grow wealth over time. That gap leaves millions of people anxious, confused, and living paycheck to paycheck — not because they’re bad with money, but because nobody ever showed them the basics.

This article changes that. Below, we break down the 5 essential components of personal finance in plain, jargon-free language. Whether you’re just starting out or looking to sharpen your financial habits, these five pillars form the foundation of every healthy money life.

64%

of Americans live paycheck to paycheck

$90K+

average US household debt (excl. mortgage)

1 in 3

adults have zero retirement savings

These numbers aren’t meant to scare you. They’re there to show you why understanding personal finance matters — and why starting today, even with small steps, can completely change your financial future.

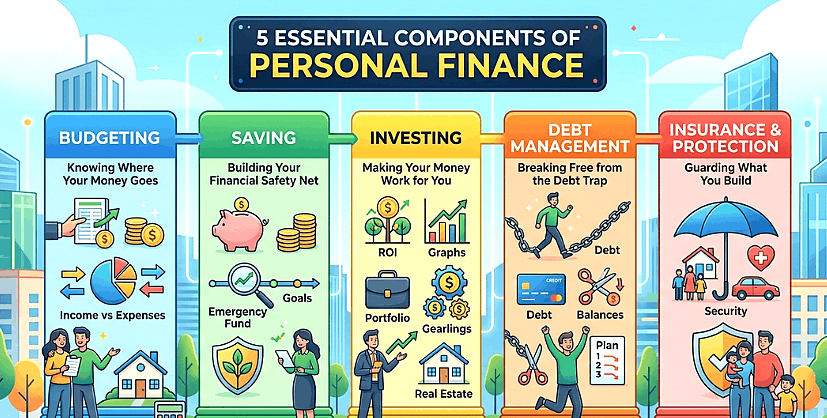

1. Budgeting — Knowing Exactly Where Your Money Goes

If you’ve ever reached the end of the month wondering where your paycheck disappeared, you’re not alone. Most people have a rough idea of what they earn but almost no idea where it actually goes. That’s where budgeting comes in. A budget is simply a plan for your money. It tells your money where to go before the month starts, rather than wondering where it went after it’s over. Think of it as your financial GPS — without it, you’re just driving around hoping you don’t run out of fuel.

The 50/30/20 Rule — The Simplest Budget Framework

One of the most beginner-friendly budgeting methods is the 50/30/20 rule. Here’s how it divides your after-tax income:

🏠 50% — Needs

Rent, groceries, utilities, transportation, minimum loan payments. These are non-negotiable expenses you must pay to live.

🎬 30% — Wants

Dining out, streaming services, hobbies, vacations. Fun things that make life enjoyable but aren’t strictly necessary.

💰 20% — Savings & Debt Payoff

Emergency fund, retirement contributions, extra debt payments. This is how you build longterm wealth.

Quick tip: You don't need a fancy app to budget. A simple spreadsheet — or even a notebook — works perfectly fine when you're starting out. The tool matters less than the habit.Budgeting isn’t about restricting your life. It’s about giving yourself permission to spend on what matters while cutting waste you probably won’t even miss. Most people who start budgeting are surprised by how much money was quietly leaking out through subscriptions, impulse buys, and daily habits they never tracked.

2. Saving — Building the Financial Safety Net That Changes Everything

Saving money is not about hoarding cash or living like a monk. It’s about building a cushion between you and life’s inevitable surprises — a car breakdown, a medical bill, a sudden job loss. Without savings, one bad event can spiral into months of financial stress. There are two types of savings that every person needs to understand:

Emergency Fund — Your Financial First Line of Defense

This is money set aside specifically for unexpected expenses. The standard recommendation is to save 3 to 6 months’ worth of living expenses. If that sounds impossible right now, start with a goal of $1,000. That single buffer prevents the majority of small financial emergencies from becoming credit card debt.

Goal-Based Saving — Saving With a Purpose

Beyond your emergency fund, you’ll want to save for specific goals: a house down payment, a new car, a vacation, or your child’s education. The key here is to keep these savings separate from your everyday checking account. When savings are too easy to access, they’re too easy to spend.

✓ Open a dedicated high-yield savings account for your emergency fund

✓ Automate your savings — set up an auto-transfer on payday so the money moves before you can spend it

✓ Label your savings accounts by goal (e.g., “House Fund,” “Emergency Fund”) — research shows this simple trick reduces unnecessary withdrawals

✓ Aim to save at least 10–20% of your income across all savings goals

The golden rule of saving: Pay yourself first. Treat your savings contribution like a bill — non-negotiable, paid before anything else. This one mindset shift is responsible for more wealth built than any investment tip.3. Investing — Putting Your Money to Work So You Don’t Have To

Saving keeps your money safe. Investing grows it. This distinction is crucial — and it’s one that most people misunderstand for years, sometimes decades. Here’s the hard truth: money sitting in a regular savings account actually loses value over time because inflation erodes its purchasing power. If your savings account earns 1% annually but inflation is running at 3%, you’re effectively getting poorer by 2% each year. Investing is how you beat inflation and build real wealth.

The Magic of Compound Interest

Albert Einstein is often (perhaps apocryphally) credited with calling compound interest the “eighth wonder of the world.” Whether he said it or not, the math is genuinely astonishing. If you invest $200 per month starting at age 25 with an average 8% annual return, by age 65 you’d have over $700,000. Wait until 35 to start and that same $200/month yields only around $300,000. Time is the most powerful variable in investing — far more than the amount you invest.

Where Beginners Should Start Investing

🏦 Employer 401(k) or Retirement Account

If your employer offers a match, always contribute enough to get the full match. This is essentially free money — a guaranteed 50–100% return on that portion of your contribution.

📈 Index Funds & ETFs

Low-cost index funds (like those tracking the S&P 500) give you instant diversification. They outperform the majority of actively managed funds over the long run and require zero stockpicking skill.

💼 Roth IRA or Traditional IRA

Individual retirement accounts offer powerful tax advantages. A Roth IRA, funded with after-tax money, grows tax-free — meaning you pay zero taxes on the withdrawals in retirement.

You do not need to be rich to start investing. Many apps today allow you to start with as little as $1. The habit and the time horizon matter far more than the starting amount.4. Debt Management — Breaking Free from the Debt Trap

Debt is one of the most emotionally heavy topics in personal finance. It causes stress, limits choices, and can feel inescapable. But here’s what most people don’t realize: not all debt is created equal. Understanding the difference between good debt and bad debt changes how you approach your entire financial life.

Good Debt vs. Bad Debt

Good debt is borrowed money that can grow your wealth or earning power — a mortgage on a home that appreciates in value, or a student loan for a degree that increases your income. These debts, managed responsibly, can be tools for building wealth.

Bad debt is high-interest borrowing used to buy things that lose value immediately — credit card balances, payday loans, buy-now-pay-later schemes for consumer goods. This type of debt actively drains your wealth because the interest compounds against you.

Two Proven Methods to Pay Down Debt

⚡The Avalanche Method

Pay the minimum on all debts, then throw every extra dollar at the debt with the highest interest rate first. This saves the most money in interest over time — the mathematically optimal approach.

🌨 The Snowball Method

Pay the minimum on all debts, then put extra money toward the smallest balance first. Once it’s gone, roll that payment to the next smallest. The quick wins build motivation — and research shows many people stick with it better.

Neither method is wrong. The best strategy is whichever one you’ll actually stick to. Many financial coaches recommend the snowball method for anyone struggling with motivation, and the avalanche for disciplined savers who are purely focused on numbers.

Your credit score matters: Your credit score affects your ability to rent an apartment, get a car loan, and qualify for a mortgage — and at what interest rate. 5. Insurance & Protection — Guarding Everything You’ve Worked to Build

Here’s a component that most personal finance beginners completely overlook: protection. You can budget perfectly, save diligently, invest wisely, and pay off all your debt — and then one catastrophic event (a serious illness, an accident, a house fire) can wipe out years of progress in a matter of months. That’s exactly what insurance is designed to prevent.

Insurance is not an investment. It’s not meant to make you money. It’s meant to prevent financial disaster. Think of it as the walls around everything you’ve built.

The Essential Types of Insurance for Most People

✓ Health Insurance: Medical emergencies are the #1 cause of personal bankruptcy in many countries. Even a basic health plan dramatically reduces this risk.

✓ Life Insurance: Essential if anyone depends on your income — a partner, children, or aging parents. A simple term life policy is affordable and straightforward.

✓ Disability Insurance: Often overlooked, yet statistically you’re more likely to become temporarily disabled than to die during your working years. This replaces a portion of your income if you can’t work.

✓ Renter’s or Homeowner’s Insurance: Protects your belongings and property against theft, fire, and liability claims. Often required by landlords or mortgage lenders anyway.

✓ Auto Insurance: Required by law in most places, but also genuinely important protection against accidents, theft, and liability.

How much coverage do you need? A good rule of thumb is to carry enough coverage so that if the worst happened, you wouldn't be financially ruined. Work with a licensed insurance advisor to review your specific situation — it's usually a free consultation.The right insurance coverage for you depends on your life stage, family situation, job type, and assets. A single 25-year-old with no dependent has very different needs from a 40year-old with a mortgage and two kids. The point is to have the conversation and make an informed decision — not to assume you’re covered when you’re not.

Frequently Asked Questions

Q: What is the most important component of personal finance for a beginner?

A: Budgeting is the foundation. Before you can save, invest, or pay off debt effectively, you need to understand where your money is actually going. Once you know that, everything else becomes much more manageable.

Q: How much of my income should I save each month?

A: A common starting target is 20% of your take-home pay, split between an emergency fund and longterm savings or retirement. If 20% isn’t realistic right now, start with whatever you can — even 5% is better than nothing, and you can increase it over time.

Q: Should I pay off debt or invest first?

A: It depends on the interest rates. If your debt carries a higher interest rate than your expected investment returns (typically anything above 6–7%), prioritize the debt. Always grab employer 401(k) matching first — that’s a guaranteed 100% return.

Q: Is it possible to build wealth on a low income?

A: Absolutely. Wealth is built through consistent habits over time, not through a single high income. Many people with modest incomes retire comfortably because they started early, spent mindfully, and invested consistently. Time and habit beat income almost every time.

Final Thoughts:

Your Financial Life Starts With One Step You don’t have to overhaul everything overnight. The truth about personal finance is that it’s built one small decision at a time — opening that savings account today, setting up that budget this weekend, making one extra debt payment this month. The five components covered here — budgeting, saving, investing, debt management, and insurance — aren’t complicated theories. They’re practical habits that, when done consistently, genuinely transform financial lives. The people who master their money aren’t necessarily smarter or higher-earning. They simply started, kept going, and learned along the way.

You can do the same. And the best time to start is right now.