Building a $100,000 investment portfolio sounds like a milestone reserved for high earners, seasoned investors, or people who got lucky with a booming stock. In reality most people don’t fail at investing because they pick the wrong stocks. They fail because they never actually start—or they start without a plan and quit when things get uncomfortable.

The first $100,000 matters because it changes the math. Once your portfolio reaches that level, market growth begins contributing meaningful amounts to your wealth. Your money starts working harder than your monthly contributions.

This guide walks you through exactly how to build a $100,000 investment portfolio from scratch, the mechanics, and the strategy that separates people who hit that milestone from those who never do.

Why the First $100,000 Is a Wealth Building Milestone

Financial commentators have long described the first $100,000 as the hardest milestone to reach. The reason is simple: Once you cross it, compound interest starts doing heavy lifting you simply can’t replicate with savings alone.

Here’s what the math looks like in practice. If you invest $1,000 per month at an average annual return of 8%—roughly in line with the historical average of a broad U.S. equity index—you’d reach $100,000 in approximately seven years. But after that point, the same $1,000/month contribution might only represent 30% of your portfolio’s annual growth. The portfolio starts feeding itself.

Once you reach six figures, however, a 10% market gain can add $10,000 to your portfolio in a year. Suddenly, compound growth becomes visible.

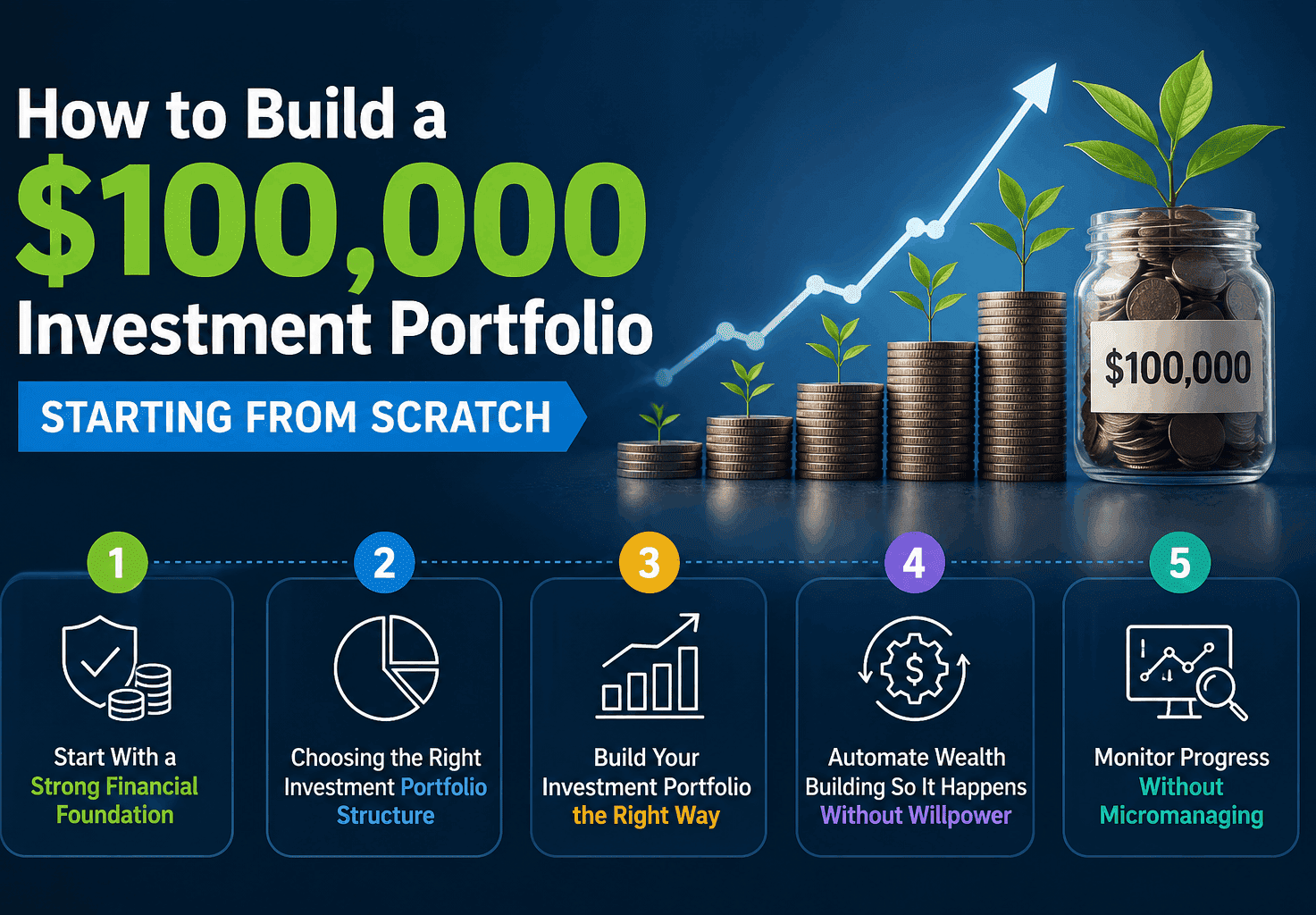

Step 1: Start With a Strong Financial Foundation

Before you put a single dollar into an investment portfolio, you need to answer two questions honestly.

Do you have debt with a high interest rate? Credit card debt carrying 19–24% APR will reliably destroy any returns a diversified portfolio generates.

Prioritize paying off:

- Credit card debt

- Payday loans

- High-interest personal loans

Do you have an emergency fund? Three to six months of living expenses in a high-yield savings account is non-negotiable before investing.

A practical target is:

- 3–6 months of essential expenses

- Kept in a high-yield savings account

- Easily accessible

This isn’t financial standard. It’s the actual reason most new investors fail: they start investing without a foundation, panic during a correction, and lock in losses they didn’t need to take.

Step 2: Choosing the Right Investment Portfolio Structure

One of the biggest mistakes beginners make is overcomplicating investing. Where you invest is often more important than what you invest in, at least in the early years.

Tax-Advantaged Accounts Come First

If your employer offers a 401(k) with a match, that match is an automatic 50–100% return on your contributions. No investment in the world reliably beats free money. Contribute at least enough to capture the full match before doing anything else.

Next comes a Roth IRA. The 2024 contribution limit is $7,000 per year (or $8,000 if you’re over 50). A Roth grows tax-free—meaning you pay taxes on contributions now, but every dollar of growth is yours to keep in retirement. For most people building wealth, especially those early in their careers, Roth accounts are the single best tool available.

Only after maxing tax-advantaged accounts should you consider a taxable brokerage account for additional investing.

HSAs: The Hidden Gem

If you have access to a Health Savings Account through a high-deductible health plan, max it out before your taxable brokerage. HSAs offer a triple tax advantage: contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, they function like a traditional IRA.

Step 3: Build Your Investment Portfolio the Right Way

Professional portfolio managers often focus more on asset allocation than individual securities. What you need is a philosophy—one you can stick with across bull markets, bear markets, and everything in between.

Start With Broad Market Index Funds

The research on active fund management is brutally clear: over 15-year periods, roughly 88% of actively managed funds under perform their benchmark index, according to S&P Dow Jones Indices’ SPIVA reports. The implication isn’t subtle. For most investors, especially those building their first $100K, low-cost index funds outperform almost everything else.

A simple three-fund portfolio covers the essentials:

- U.S. Total Stock Market Fund (e.g., VTI or FSKAX) — broad domestic equity exposure

- International Stock Market Fund (e.g., VXUS or FTIHX) — non-U.S. developed and emerging markets

- U.S. Bond Market Fund (e.g., BND or FXNAX) — stability and income

The allocation between these depends on your age and risk tolerance. A common starting point for someone in their 30s is 80% stocks (split ~60/40 between U.S. and international) and 20% bonds. Adjust as you approach retirement.

Don’t Ignore Expense Ratios

A 1% annual expense ratio on a $100,000 portfolio costs you $1,000 per year—and that’s before the compounding you lose on that $1,000. Vanguard, Fidelity, and Schwab all offer broad index funds with expense ratios under 0.05%. That gap sounds trivial. Over 30 years, it isn’t.

Rebalance, But Don’t Obsess

Once a year—or when an asset class drifts more than 5–10% from your target allocation—rebalance. Doing it more frequently often incurs unnecessary transaction costs and tax drag in taxable accounts. Automating contributions to underweighted funds is a cleaner approach than selling overweighed ones.

Step 4: Automate Wealth Building So It Happens Without Willpower

The biggest predictor of long-term investing and wealth building success isn’t intelligence, income, or market knowledge. It’s consistency. And the best way to be consistent is to make consistency effortless.

Set up automatic contributions on payday—before the money lands somewhere else. Increase contributions by 1% each year, ideally timed to any raise you receive. A raise you never fully see in your take-home is a raise you’ll never miss.

This is not a joke. A Fidelity analysis found that investors who had accounts during the 2008–2009 crash and did nothing at all outperformed investors who made active changes. Automation builds that inertia in your favor and supports long-term wealth building.

Step 5: Monitor progress without micromanaging

It is harmful to your investing portfolio to check it every day. Short-term volatility will be seen as proof that anything is wrong, even though it virtually never is. Markets have traditionally plummeted by more than 20% every five to seven years, but have always recovered.

Use quarterly check-ins to assess your allocation, ensure contributions are going to the correct accounts, and adjust your aim if your life circumstances have changed. Annual reviews are the ideal time to address more in-depth strategic concerns.

Tools worth using: Personal Capital (now Empower) provides a comprehensive net worth view, while your brokerage’s built-in dashboard allows for portfolio management.

Common Investment Portfolio Mistakes

Building wealth isn’t only about making good decisions.

It’s also about avoiding destructive ones.

Trying to Time the Market

Research consistently shows that missing only a handful of the market’s best days can severely reduce long-term returns.

Investors who wait for the “perfect entry point” often remain on the sidelines.

Chasing Hot Investments

Every cycle produces fashionable investments.

- Technology stocks.

- Cryptocurrencies.

- Artificial intelligence companies.

Some succeed. Many disappoint.

A diversified investment portfolio reduces dependence on any single trend.

Ignoring Fees

A seemingly small 1% annual fee can cost tens of thousands of dollars over several decades.

Focus on:

- Low-cost index funds

- Low expense ratios

- Tax-efficient investing

Small costs compound just like gains.

Selling During Market Crashes

The stock market has experienced declines of 20%, 30%, and even 50%.

These periods feel terrifying in real time.

Historically, however, markets have recovered and reached new highs.

Investors who remain disciplined often benefit the most from eventual recoveries.

A Sample $100,000 Portfolio Plan

Let’s assume:

- Age: 30

- Investment horizon: 25+ years

- Moderate risk tolerance

Sample allocation:

Stocks (80%)

- 55% U.S. Total Market Index Fund

- 25% International Index Fund

Bonds (20%)

- 20% Total Bond Market Fund

Monthly contribution:

- $750

Expected long-term return:

- Approximately 7–9% annually

Potential timeline:

- Around 8 years to reach $100,000

Of course, actual results vary. Markets don’t deliver smooth annual returns. Some years are exceptional. Others are disappointing.

The key is maintaining consistency regardless of market conditions.

Conclusion

Building a $100,000 investment portfolio from scratch is less about finding extraordinary investments and more about following a repeatable process.

Start with a solid financial foundation. Eliminate expensive debt. Create an emergency fund. Invest consistently in diversified assets. Focus on asset allocation rather than speculation. Increase contributions whenever possible.

The path to wealth building isn’t perfectly linear. Markets will rise, fall, and test your patience. Yet history has repeatedly rewarded investors who stay disciplined and keep investing through uncertainty.

The first $100,000 may take years to achieve, but once you cross that threshold, compound growth becomes a powerful ally. Start today, automate the process, and let time do the heavy lifting.